October finances businesses during all important moments in their growth. Such as renovating the office, taking over another business, or investing in a clever CRM system. You can imagine that these different Moments of Life call for different types of loans. In addition to the standard amortisation scheme, October also offers other financing solutions. This has implications for the repayments of your loans.

Different types of loans

In addition to the standard loan, where capital and interest are paid monthly through annuities, October also offers a flexible loan and an extended loan.

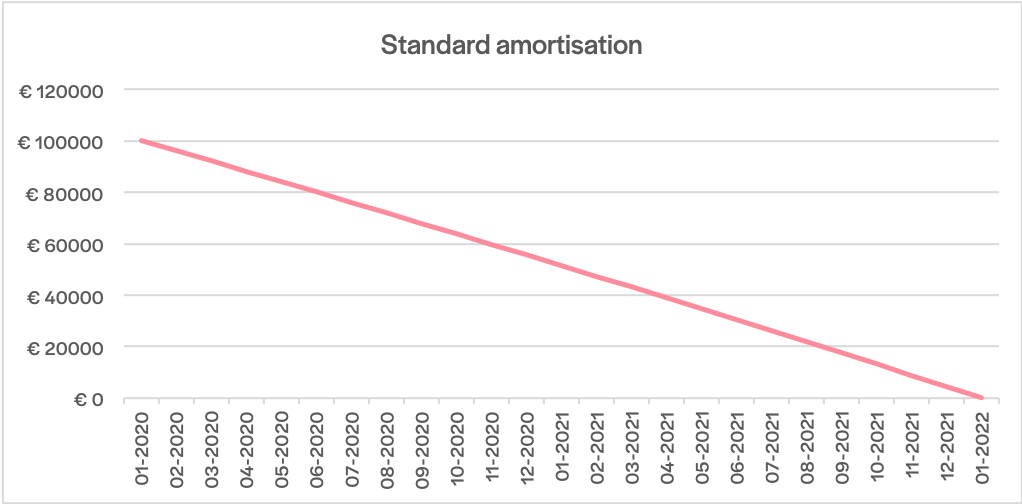

As a reminder, here’s an example of the repayment scheme of a standard loan of €100,000 over 24 months:

The flexible loan

When a company needs financing quickly and is able to repay the loan shortly afterwards, a flexible loan offers a solution. This allows the company to repay early, at no extra cost.

A flexible loan, is a loan with a standard amortisation. The company has the option of repaying the loan in full at any time after 9 months. However, it is not an obligation; the company can also repay the loan according to the original repayment schedule.

If the borrower opts for a flexible loan, this will be specified in the project description. When you invest in this project, after 9 months you can receive a message that the project will be fully repaid at any time. You will receive the remaining outstanding amount within a few days on your October account.

If a borrower does not opt for a flexible loan, but does repay the loan early, the company will pay a penalty of 4% of the outstanding amount. 2% goes to the lenders and 2% goes to October.

Summarised:

✔️ The borrower can repay early after 9 months at no extra cost.

✔️ The lender receives the full outstanding amount at once on theirOctober account.

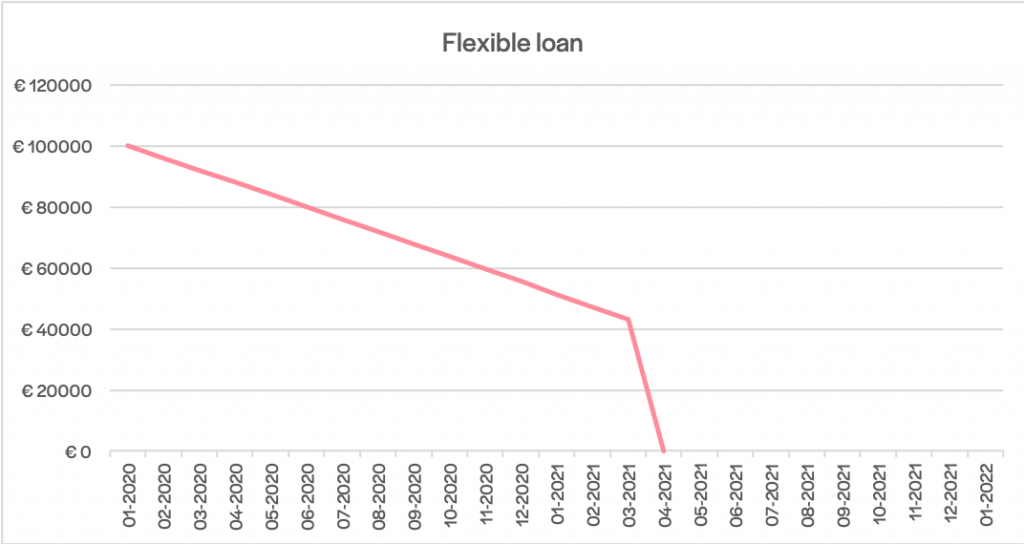

Example of the repayment scheme of a flexible loan loan of €100,000 over 24 months, that is repaid early:

The grace period

Sometimes it is not suitable for a company to start repaying the loan immediately. For example, the opening of a new office or after a major renovation, can put a strain on the cashflow. Or maybe the loan is used to purchase new machinery, which only start to realise their full potential after a few months. If a company expects not to generate enough turnover at the start of the loan, a grace period offers a solution. During the grace period, only interest is paid and no capital repayments take place.

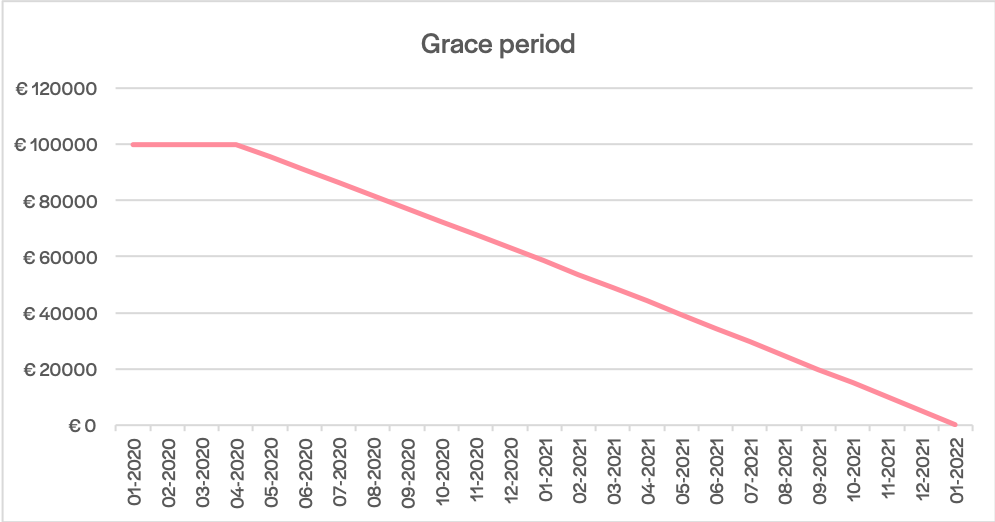

Example of the repayment scheme of a loan of €100,000 over 24 months, with a grace period of 3 months:

The extended loan

In addition to the flexible loan, a company can now also make use of an extended loan. This loan is characterised by the grace period of 12 months and a higher final repayment. During this grace period, the entrepreneur only pays interest to the lender. Because no repayments have yet been done, the monthly interest payment remains high.

After the grace period, relatively small monthly capital repayments take place. These payments are not sufficient to pay off the loan within the term. As a result, the borrower makes a final payment to repay the remaining amount at once. This is normally between 15% and 30% of the loan amount.

Summarised:

✔️The company has a grace period of 12 months, the lender only receives interest on the principal amount.

✔️After the grace period relatively small monthly repayments take place, the lender receives repayments and interest.

✔️The company repays the remaining outstanding capital at once at the end of the term, the lender receives a higher repayment than in previous months.

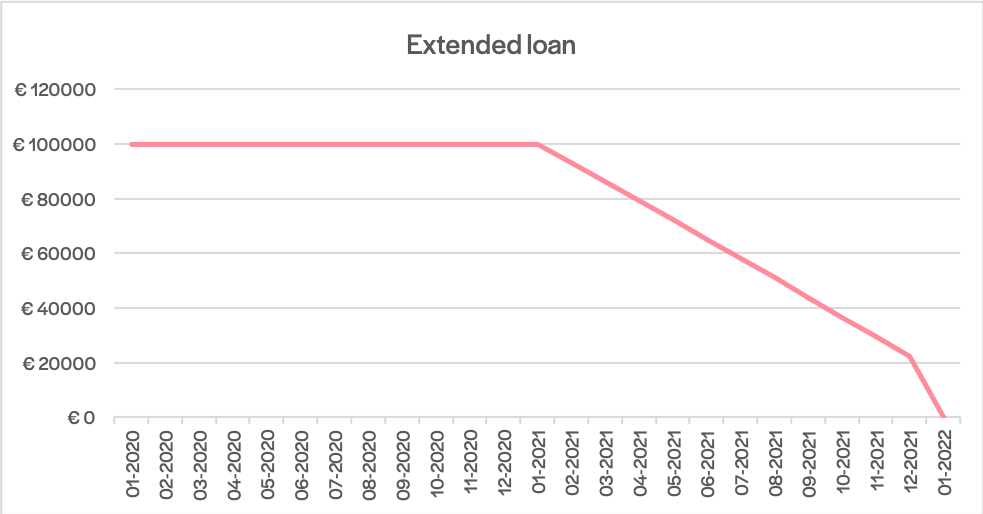

Example of the repayment scheme of an extended loan of €100,000 over 24 months:

How to manage

In the project description we will always mention the type of loan. Before you make an investment, you will be able to access the repayment schedule of the loan. In your portfolio you can keep track of the repayments you will receive each month and how much capital is still outstanding in each of your loans.