When you lend to a company on October, your loan is mostly repaid monthly through annuities. In this blog we will tell you about the characteristics of an annuity loan and what are the upsides compared to other types of loans.

What is an annuity loan?

Distinctive for an annuity loan is that it is repaid monthly by a fixed amount. The fixed monthly repayment is a sum of interest and capital, with the same amount as outcome for the duration of the loan: the annuity.

However, the ratio of interest and capital within the annuity changes over time. As with any loan, a company only pays interest on the outstanding amount. So, at the start of the loan the ratio of interest is larger, because the outstanding amount is still relatively high. Over time, the ratio of interest in the annuity decreases, as the amount of outstanding capital over which interest is paid decreases.

Because the loan is repaid through a fixed amount, it means that the ratio of capital repayments within the sum has to increase. So near the end of the maturity of the loan, the company repays mainly capital and only a small portion of interest. The development of the ratio of interest and capital over the duration is shown in the repayment schedule below.

What are the benefits of an annuity loan?

The annuity loan has some benefits over other types of loans for the lender, as well as for the borrower. For the lender an annuity loan is:

- Easy to understand and transparent,

- A constant and predictable cashflow,

- More profitable than other types of loans (see an example below).

Besides easy to understand, transparent and predictable, for borrowers an annuity loan is:

- A lower burden on the cashflow at the start of the loan, compared to other types of loans.

How does it compare to a linear loan?

The best-known type of loan is the linear loan. It is a type of loan that has equal capital repayments for the duration of the loan. Interest is paid over the capital that has not been repaid yet: the outstanding amount.

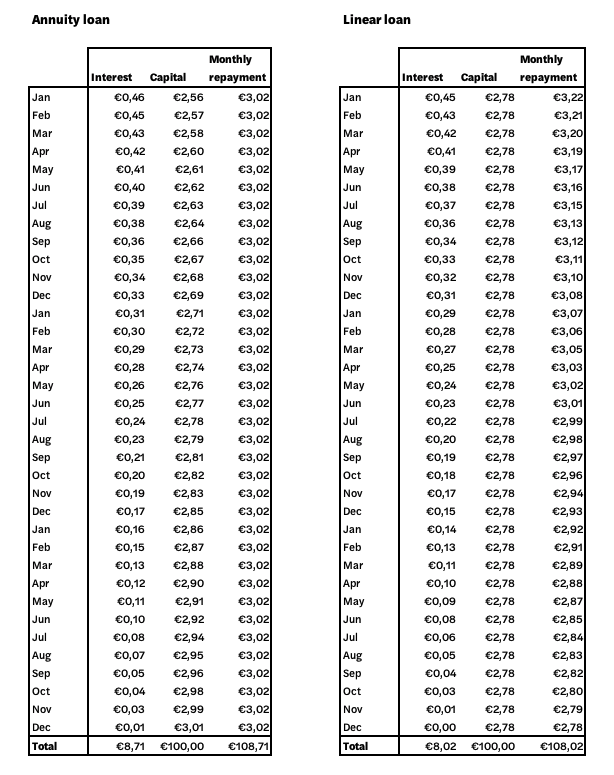

In the table below you can see how the the two types of loans, linear and annuity, compare. For the example we take a project that has an interest rate of 5.5% and a duration of 36 months. The invested amount is €100.

As you can see, with both types of loans after 36 months the loan is fully repaid. With an annuity loan a lender would have been paid €8.71 in interest, with a linear loan a lender would have been paid €8.02. This difference results from a higher outstanding amount for a longer duration, leading to more interest paid. The annuity loan is €0.69 more profitable than a linear loan; a difference of 8.6% over 36 months.