Today, thanks to the growing development of FinTech sector, people have access to a series of increasingly innovative tools to manage their investments. One of these is crowdlending. Crowdlending is a relatively new financial product (less than 10 years in Continental Europe), which offers individuals the opportunity to stream their savings to SMEs. Thereby lenders support the real economy. The return on their investment comes in the form of interest.

But, is the yield the main reason for people to start crowdlending? We asked our most active lenders, with a portfolio of at least 10 different projects, about their motivations. Over 350 lenders, equally divided over France, Italy, Spain, and international nationalities, completed the survey.

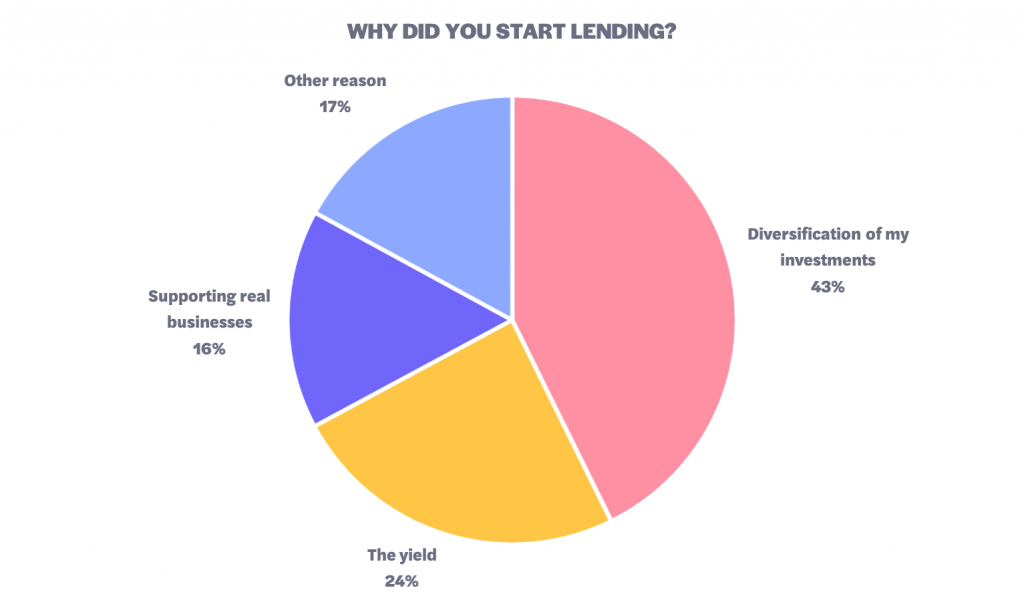

Third place: supporting companies

With 16% of the answers, the support of companies was the third most mentioned reason to start crowdlending.

What makes crowdlending unique is the ability to make a return on your savings, while supporting the real economy at the same time. With their loans, lenders empower companies to grow, which makes the direct impact of an investment tangible.

We previously thought that this would be a bigger motivator in the decision to start crowdlending.

Second place: the yield

Many lenders move towards crowdlending because of the higher yield it offers when compared to classic bank savings. It was the second most mentioned reason to start lending with 24% of the answers.

Back in 2014, the European government started to change regulations and broke the monopoly of banks on SME credit. This allowed private investors to lend directly to companies and take on the role of the bank in this profitable asset form. Platforms like October facilitate transactions and have reduced the entry barriers for investors. The platforms select projects for investors and allow them to review the goals of the project and to learn what the money will be used for. If an investor supports the project, they just have to select the amount of their loan. After that, the lender can cross his or her arms and wait for the loan to be repaid with interest.

At the time of writing, the October portfolio as a whole has an internal rate on investment of 4.61%. This is after defaults and free of costs. This and more performance indicators can be found in our statistics, which we update monthly.

First place: diversification

We were surprised by the most mentioned reason to start crowdlending: “to diversify my investments” makes up 43% of the responses.

This implies that a large part of the people who start crowdlending already invest in other financial assets. As they should! Holding a diverse portfolio of financial products allows the yield of your portfolio to be more stable. For example, the value of an investor’s stocks may take a hit when new trade sanctions are placed on China, but their loans to an SME based in Europe will not be (directly) affected. When an investor holds a portfolio of multiple financial products, the portfolio is less dependent on the economic trends of that financial product.

Moreover, with recent technological advancements and changes in regulation, access to different financial products has become easier. A good example includes crowdlending: on October, it is possible for a lender to sign a loan contract with a company with just a few clicks. It is even possible to create a loan from the palm of your hand using a smartphone. A couple of years ago this was unimaginable.

Within crowdlending, it is possible to diversify your loan portfolio as well. From only €20 per loan, a lender can lend to a company on October. This makes it possible to spread an investment over several smaller loans. As a result, the impact on the return in the event of a default is smaller and the loss of capital is less significant. When an investor spreads the investment over several sectors, risk categories, and loan maturities, the loan portfolio is also less dependent on the economic status of a country or sector.