In June 2019, October’s Chief Risk Officer Marc Sebag answered lenders’ questions on defaults and the continuous improvements of our scoring model. A little more than a year later, the pandemic and the economic slowdown which followed have changed the landscape for SMEs. In today’s interview, Marc shares his thoughts on the impact of Covid-19 on the portfolio, October’s support for SMEs through the crisis and the changes implemented on the platform to adapt to the new reality.

1. What has been the impact of the Covid-19 on European SMEs?

When the Covid-19 crisis began, most SMEs including those in our portfolio started facing immediate cash flow issues, as they had to suspend their activity, reduce their production, or anticipated a drastic economic slowdown. To give you an idea, the European Economic Forecast Summer 2020 estimated that the Euro Area operated at 25 to 30% of its capacity during the lockdown, with some sectors being totally stopped. This was both a supply and a demand shock, extremely sudden, the likes of which the world had never seen.

At the beginning of March we received many calls from our borrowers, first in Italy and then in other countries where October operates, requesting payment holidays to preserve cash in this uncertain context. In particular, hotels, bars and restaurants were forced to close. These companies could not maintain the same level of activity but they still had to pay their employees, supplier bills, taxes and financial creditors.

To answer that need, European governments launched exceptional measures (state guarantee schemes, furlough plans, tax holidays…) to provide liquidity to companies and give them time to get back on their feet. Banks, but also lending platforms such as October, participated in this support program and continue to do so.

2. What specific actions did October carry out to quickly support SMEs ?

Since the beginning of the pandemic, our goal has been to give companies the best chance to stabilise their financial health, restart their activity, and put them in a position to repay their loans in the future.

In March, October proposed to freeze all borrowers’ capital repayments for a period of three months (April, May and June 2020) to give them breathing space and protect the interest of all the October lenders, who voted overwhelmingly in support of the freeze. 98% of companies managed to fulfil their commitment to pay interests during this period. And October also froze its monthly fees, as an additional alignment of interest.

After these 3 months, for companies operating in the sectors most affected by Covid-19 (tourism, events, restauration, fitness…), we renewed the freeze of capital repayments for periods from 3 to 9 months, with prior approval from lenders. 10% of our borrowers requested that extra capital freeze.

We received positive feedback from our community of retail lenders, institutional investors, and borrowers. I take this opportunity to thank you again for your trust and strong support.

3. The 3-month capital freeze was an immediate short-term answer to the crisis, but how did you adapt your model in the following months and what is the current situation in each country?

A lot has been implemented in terms of operations, credit and technology.

In fear of a credit crunch and eventually the bankruptcy of SMEs, governments have been reducing the risk for lenders with state guarantees. According to the applicable law, October participates in the French, Italian and Dutch state guarantee programs. Let’s see how they work:

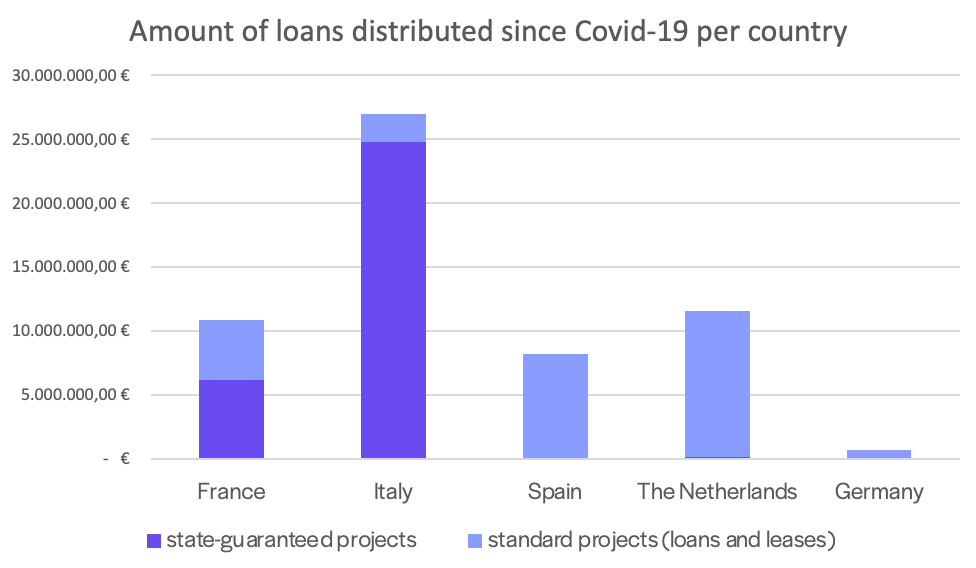

In France, borrowers benefitting from the French State guarantee initially receive a 12-month deferred loan at 2%, which can be extended up to 5 years with a higher interest rate. The guarantee covers 90% of the outstanding capital in case of default. As of end of September, 34 guaranteed deals have been financed on the platform for a total amount of € 6.1M.

In Italy, the “Fondo di Garanzia PMI” guarantee scheme put in place by the Italian government only applies to loans financed exclusively by institutional investors and covers up to 90% of the outstanding capital. October actively participates in this program to:

- Refinance elegible loans of our existing portfolio. Supported by retail lenders through a vote in April 2020, this measure allowed borrowers to get additional liquidity with a longer reimbursement period and retail investors to be fully repaid. To date, more than 23 projects were refinanced for a total amount of €4,9M representing around 38% of the overall eligible Italian portfolio.

- Grant new loans to Italian borrowers elegible to the guarantee. By the end of September, 108 Italian SMEs received a state-guaranteed loans and € 24M were distributed through the October platform.

In The Netherlands, October participates in the Dutch State guarantee program. The guarantee is only made available to eligible companies once other government measures have been used, and covers approximately 65% of the outstanding capital. So far, one Dutch state-guaranteed loan of €160.000 was financed on October by both retail and institutional lenders.

In Spain and Germany, where lending platforms are not allowed to participate in state guarantee programs, October continues to support SMEs with non-guaranteed loans, based on a thorough credit analysis to assess the impact of Covid-19 and the timeline to go back to a certain level of normality.

From March 1st, 2020 to September 30th, 2020.

4. How are you coping with the high volume of state-guaranteed loan requests coming in?

October has built a predictive risk score, Magpie, to respond to them instantly. Magpie is built using machine learning tools on large amounts of data collected by October over the past 5 years across different countries; it estimates the risk of default of companies and is specifically tailored to our borrower population. Projects under €250,000 covered by a state guarantee can be assessed instantaneously, offering a fast and simple experience to borrowers and more opportunities to diversify for lenders. These are called Instant Projects.

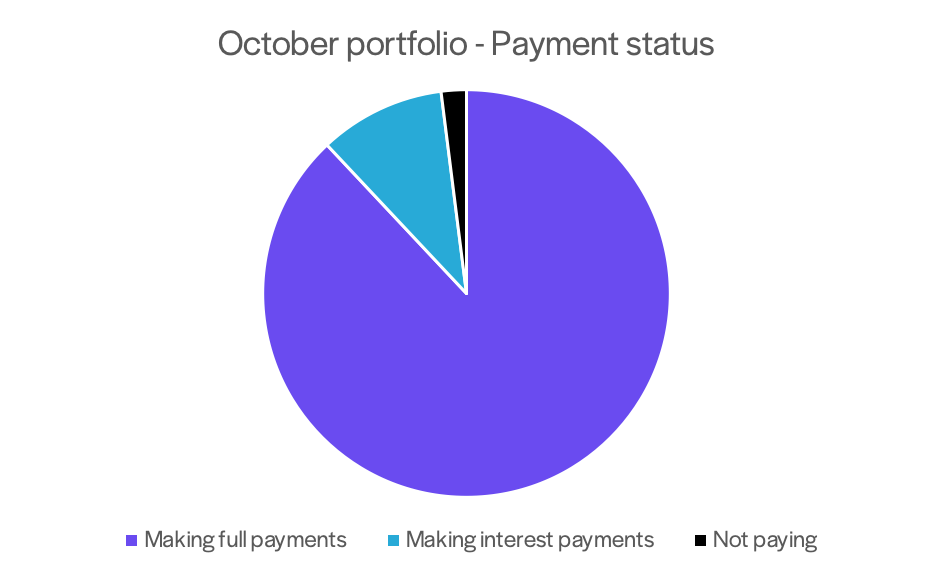

5. What has been the impact of Covid-19 on repayments?

Thanks to our proactive measures, most companies kept making their monthly repayments normally. In July, after the end of the 3-month capital freeze, 98% of our borrowers who were not in default before Covid-19 paid their monthly repayment without any incident. 88% of these companies are repaying the full instalment (both capital and interest) and 10% pay only interest, as they belong to the group of borrowers most impacted by the crisis that was granted an extra capital freeze.

As of September 2020, excluding projects in default previous to Covid-19

6. More generally, what is the situation of the global October portfolio today in terms of defaults?

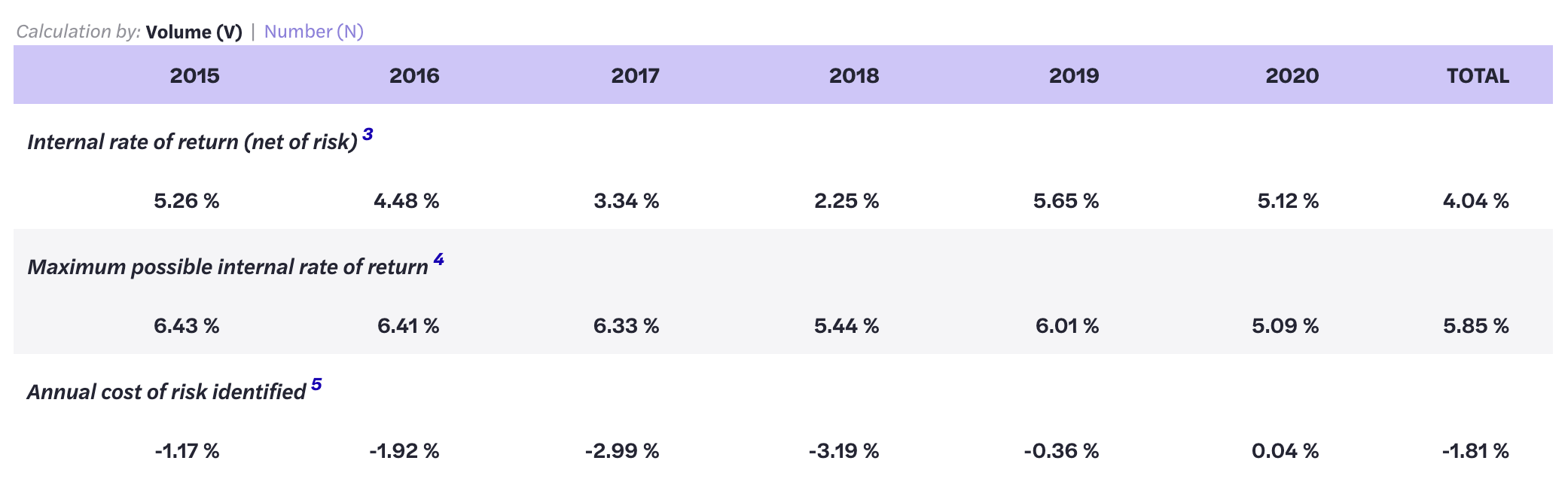

On our statistics page, you can find at any moment the impact of defaults on the October portfolio. As of today, you can see that, for a portfolio made of all the projects ever published on October, the internal rate of return (IRR) post-default is of 4.04% (vs. an IRR before default of 5.85%).

As of September 2020, in volume. Annual cost of risk (difference between initial IRR and IRR post default) was positive in 2020 due to various rescheduling.

As mentioned in my previous interview, our default rate for projects done in 2017 and 2018 started to increase. As our portfolio matured, it is normal to start having defaults after a certain period of time, but this was also a chance to learn and improve, especially on early defaults.

At that time, a portfolio analysis was performed and we focused on 4 drivers of early defaults: fraud, acquisition finance, riskier industries and geographies. (Fraud matters a lot. In particular, 97% of the amount in default of A projects is linked to one fraudulent project.)

To maintain the default rate under control, we took corrective actions to improve our scoring model such as stricter criteria and we invested more in the identification of fraud patterns. This enabled us to decrease early defaults (occurring during the first 12 months): 1,2% of the projects originated in 2019 defaulted within 12 months, following the implementation of the corrective measures (versus 3,8% in 2018).

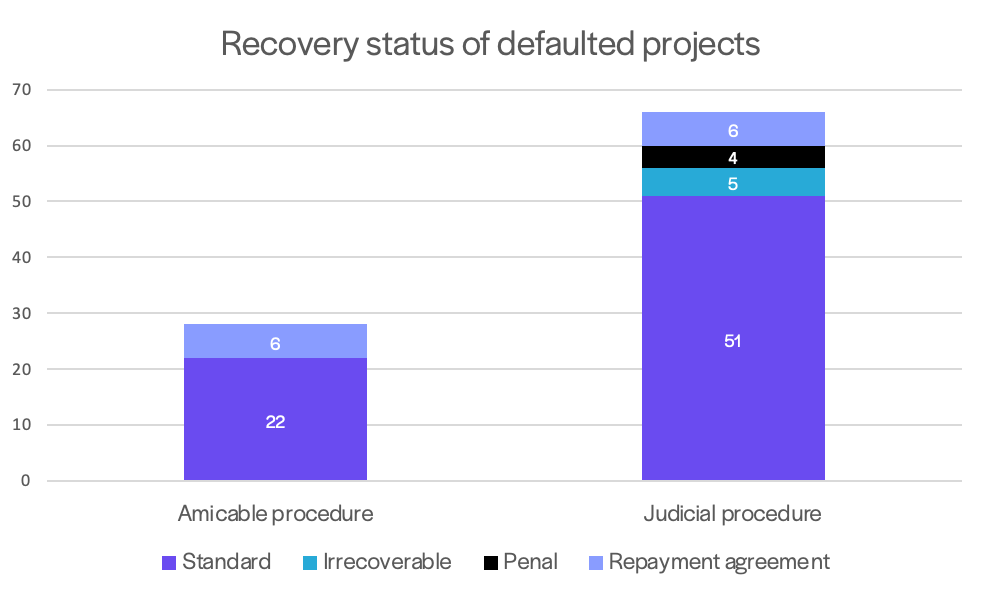

Crucially for the performance of the portfolio, October manages early recovery internally, with a cross-country team made of 6 experienced professionals, working closely with local lawyers and recovery agencies to defend our lenders’ interest. Recovery actions go from amicable to judicial procedures and can end up in penal prosecutions in case of frauds (we are currently leading penal procedures with 4 borrowers). As of today, out of the thousand projects financed on October, 66 are in judicial proceedings and 28 are in amicable recovery proceedings. Among these defaulted projects, 5 have been declared irrecoverably lost by the courts and 12 have reached a repayment agreement with October lenders.

As of September 30th, 2020, in number of projects.

7. How do you think Covid-19 will impact the October lenders’ returns?

Negatively, that much is clear; but it will take some time for the effects to become fully measureable. First, the impact of the crisis on lenders’ portfolios will depend on their level of diversification. But also, there is still a high level of uncertainty on the medium term Covid-19 economic impact.

Right now, we are still in the eye of the storm. Everywhere, states have enabled taxes and social contributions moratoriums, launched state guarantee programs… to support SMEs and employment in the next 12 months. During this time, companies may resist thanks to this variety of support programs; but trouble may start in Q1 2021, when moratoriums end and companies will have to start repaying their state-guaranteed loans.

Our Sales, Credit and Operation teams will keep on being proactive in monitoring the October portfolio through our monthly contact with borrowers for the repayments and following information provided by external databases.

8. Can you explain what has changed in terms of credit assessment following the crisis?

The credit analysis of projects that are presented on October is performed in-house. We collect quantitative and qualitative information necessary to assess the risk of a project and decide an interest rate.

We continuously improve our risk scoring model based on the evolution of our portfolio and the market. The change of paradigm caused by the coronavirus crisis obviously impacted the way we assess companies and made us implement some adjustments:

- Review of our industry classification. At October, we classify sectors in 4 categories based on the underlying risk: positive, no restriction, high vigilance, prohibited. Sectors in which the activity has become unstable due to the containment measures, such as the tourism sector or the transportation industry for example, were passed to high vigilance. This means that projects from these sectors will be submitted to a more detailed analysis. In parallel, focus will be put on some high-potential industries such as pharmaceuticals or IT, among others.

- Focus on resilient companies. To be granted an October loan, companies have to meet the following criteria:

1/ Demonstrate that they were profitable and fitted our criteria before the outbreak of coronavirus,

2/ Show a capacity to come back to a certain level of activity within the next 12 to 24 months. - Enrich the borrower questionnaire. The call conducted by the Credit analyst during the credit process has been enriched with questions aiming at assessing the resilience of borrowers. A strong emphasis is put on understanding the company’s operational ecosystem, liquidity situation and management’s capacity to adapt their business model to the current challenging situation. The goal is to have a clear picture of the borrower’s present situation, see how they foresee the coming months and the timeline to come back to ‘normality’ from a business standpoint.

- Be extra vigilant with fraud. In times of crisis, fraudsters are very active and try to take advantage of the situation. In the last year, we have strengthened our anti-fraud system developing a series of tools that are proving useful to detect fraud attempts.

We are continually reassessing the situation and will make necessary adjustments depending on how the crisis unfolds.

9. Finally, where do you see the October activity in the next 12-18 months?

Our mission stays the same: to empower SMEs by simplifying and democratising their financing. We will keep working on making entrepreneurs’ life easier and guiding them efficiently towards the source of financing that best suits them, whether it is a state-Guaranteed loan, a non-guaranteed loan or a financial lease.

Recently, we strengthened our lending capacity by raising €258M from major international institutional investors, such as Gruppo Intesa San Paolo, which will help us accompany all types of companies at every important moment of their life.

To fulfil our goal, we will move further towards data-driven and digitized credit analysis to improve our existing predictive risk tool, which is live in France, Italy, and soon Spain, and deploy our Instant Decision process on more products and markets. To do so, we are currently developing our Product, Tech and Data teams.

We hope this interview will result useful for all of you and are at your disposal on the October chat for further questions.