Save or invest, how many times have we asked ourselves this question? After the financial crisis of 2007, the interest rates guaranteed by deposit accounts fell dramatically. The majority of savers were frustrated by the sharp decline. Nonetheless, they remain committed to liquid savings, because they lack de adequate financial knowledge of other financial products.

This is what emerges from the survey carried out by J.P. Morgan on a sample from Great Britain, Belgium, Italy, Spain, Germany and Austria.

A consolidated habit

The research shows that the habits of European savers have not changed over the last decade: 8 out of 10 people qualified as savers and almost as many admitted that they did not know any financial product. Only 7% of respondents stated that they were oriented towards financial products that can guarantee a stable return.

The majority of respondents were aware of the extremely low return from deposit accounts and half said they were completely dissatisfied with the performance of their savings.

Preserving or increasing capital?

However, this dissatisfaction does not seem to translate into a reversal of the trend. 40% of the sample believes it is more important to preserve capital than to increase it. A further 30% still seems very cautious, preferring a minimum return to high volatility.

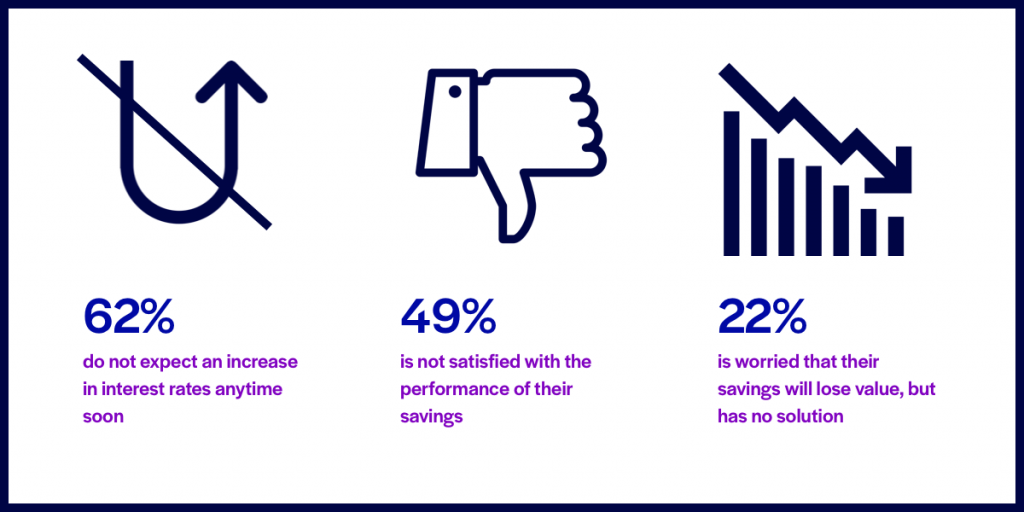

Speaking of the future, savers don’t seem to have high expectations for a possible increase in yields: 62% believe interest rates will not increase in the short term. This feeling is even more pronounced for nearly a quarter of the sample, which is worried about a possible loss of value. Despite, they don’t have a solution to increase the return.

Savers need more awareness

In general, the trend described above is caused mainly by two factors: on the one hand poor financial knowledge, and on the other hand risk aversion.

One in four people stated they had no knowledge of financial products and wanted to stay as far away from investments as possible. One in five did not approach them for fear of market fluctuations and the possible loss of capital associated. Two other categories of savers emerge from the study: those who have simply never thought of investing their savings (17%) and those who say they are interested in doing so, but are held back by the lack of reliable advice (11%).

Crowdlending: a new investment opportunity for 2019

Today, thanks to the growing development of Fintech platforms, savers have access to a series of increasingly innovative tools for managing their investments. One of these is crowdlending, which offers private investors the opportunity to stream their savings to SMEs, thereby supporting the real economy. In return, lenders can achieve attractive returns, especially when compared to other types of investments. Moreover, this innovative asset class is not subject to fluctuations in the financial markets. Thanks to their simplicity and transparency, crowdlending platforms allow private individuals to invest their savings directly and independently.

On October, lenders lend their savings directly to European SMEs, alongside institutional investors, obtaining a monthly repayment of capital and interest. October allows lenders to choose which companies to lend to: each project is published 48 hours before the opening of the subscription, so that lenders can always make an informed choice.

Lending to SMEs is not free of risk. There is a risk of capital loss and savings are immobilised.