The State-guaranteed loan is an important tool by the French government to support businesses during the covid-19 crisis and the economic emergency that followed. Since the 8th of May 2020, lending platforms like October (with the status IFP –Intermédiaire en Financement Participatif) can distribute State-guaranteed loans.

What is a French State-guaranteed loan?

It goes without saying that the covid-19 crisis has created a high level of economic uncertainty. As a result, lenders in general are less willing to provide credit. SMEs still need credit, sometimes for growth, more often in today’s environment to continue paying bills and salaries, while their income is (temporarily) dropping.

In fear of a credit crunch and eventually the bankruptcy of SMEs, governments are reducing the risk for lenders with state guarantees. With a state guarantee, the government covers a part of the loss in case a loan defaults. In other words, if a company cannot repay the loan, the state will partially repay for the company (up to 90%). As such they make it safer for you, as a lender, to lend to an SME.

A 300 billion euro package

On the 18th of March, the French State announced an exceptional package of 300 billion euro State-guaranteed loans. Initially these guaranteed loans were distributed by banks alone. Now the initiative is extended to lending platforms, which enables eligible companies to obtain a loan with a State guarantee directly on October.

With the guarantee, the French state covers 90% of the capital lent for all companies with less than 5,000 employees and a turnover of less than 1.5 billion euro. Larger companies are supported with a 70% or 80% loan. The guarantee is capped at 25% of the turnover of the company.

“This is excellent news, that will enable us to support SMEs even more actively in this difficult time. We will do this at cost price. With solidarity.” Olivier Goy, Founder and CEO of October.

October supports businesses in every way possible

October is taking proactive measures to support companies during this crisis:

- 2 months ago, we implemented an automatic 3-month freeze on capital repayments for all our European borrowers after a vote among our individual lenders and institutional investors (where they showed massive support, with 99% of them voting yes!).

- 1 month ago, October lenders offered Italian borrowers a refinancing solution allowing them to benefit from bigger loans (in amount) covered by a public or private guarantee.

- With this new initiative, we will be able to go further and finance companies with cash flow tensions with state guarantee loans.

October is normally remunerated through project set-up fees and monthly fees, that are charged to companies that lend on the platform. October will grant State-guaranteed loans at cost price for borrowers. The interest rate paid by companies that borrow on October remains totally dedicated to the remuneration of retail and institutional lenders. The interest rate will be lower, thanks to the state guarantee.

How retail lenders can participate in these projects

We have answered a dozen questions that you could have, to help you understand how you can support businesses while benefiting from a guarantee.

1. Does the guarantee cover the entire duration of the loan?

Yes the loan is covered by the State guarantee for its entire duration. Only if the company defaults within the first 2 months after granting the loan, the guarantee will not apply.

2. What are the costs for lenders?

There are no associated fees for lenders. It is the borrower who bears the cost of the guarantee. To be clear, there are never any costs for October lenders (no top-up, no debit, no management fees, etc.).

3. Is the interest rate different from a “normal” October loan?

Yes, the interest rate for a State-guaranteed loan is different from a normal October loan. There are 2 major differences in a French State-guarantee loan:

- The October rate grid is lowered. Why? Since the loan is guaranteed by the State, the cost of risk is thus lower.

- The interest rate changes during the term of the loan.

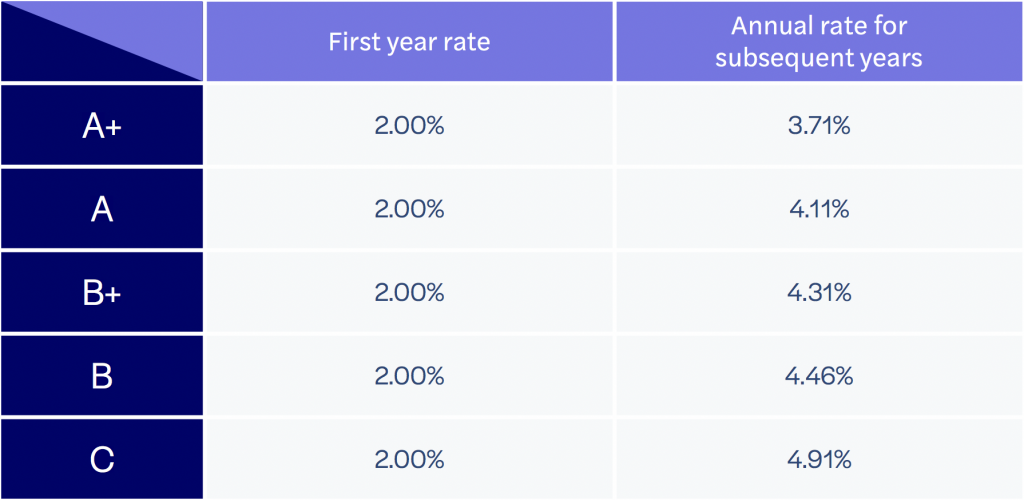

4. What is the interest rate for the lender?

For the first 12 months the interest rate of all State-guaranteed loans on the platform is 2%. During the first 11 months there is no repayment; no capital, no interest. The interest is paid in the 12th month. The borrower can also repay the capital (partially or in full) at the end of the first year.

If the borrower decides not to repay the loan in full and spread the repayment of the loan over a period from 1 to 5 years, a new interest rate is applied for the following years.

The new interest rate follows the rate grid below:

The interest rate displayed on the State-guarantee loans project page will thus be 2% and the duration 12 months. After the first year, the new interest rate will be displayed with the new duration.

5. What is the change in risk compensation for lenders?

October’s non-guaranteed interest rate grid ranges from 2.5% to 9.9%, depending on the risk of the company. For all French State-guaranteed projects, to reflect the fact that 90% of the risk is covered, the Internal Return Rate (IRR)is lower. Its exact level will depend on how long, at the end of the first year, the borrower decides to keep the loan for.

As an example if the borrower is a B+ and decides to keep the loan for 2 years after the first year (total maturity 36 months), they will pay 4.31% for the last 24 months, which translates into an IRR of 3.15% to lenders over the full life of the loan.

6. Can all lenders lend to businesses that benefit from the State-guaranteed loan?

All retail and institutional lenders can lend to State-guaranteed projects published on the platform, regardless of their country of residence.

7. How to distinguish a State-guarantee project from a “classic” project?

In the Project Description it will be indicated with the following sentence: “This project is covered by the French State Guarantee”.

8. What is the risk if a company defaults?

The state guarantee does not secure the continuance of a business. The business is merely provided with extra credit, to support the company during the coronavirus crisis. Nonetheless, no one can predict how the company will come out. In other words, your loan can default. Therefore, the risk of a State-guaranteed loan is the same as a traditional loan: you can lose part of the capital lent. The State guarantee covers up to 90% of the capital. This means that if a company goes bankrupt and no longer pays its instalments, the State will reimburse lenders 90% of the remaining capital owed by the borrower. The risk of capital loss, apart from the risk of the French government defaulting, is therefore only on 10% of the capital. It is the lender who bears the risk, just as with a “classic” October loan. The platform does not under any circumstances substitute to the borrower’s repayments.

9. When is the guarantee activated?

The guarantee is activated once a judicial officer has issued a certificate of uncollectibility for the October lenders’ debt.

This certificate is issued if none of the debt recovery initiatives have been successful. Usually the company is in judicial recovery or liquidation at that state. It can take several months or even years between the first payment default of a company and the activation of the guarantee.