The French state-guaranteed loans at a glance

On March 2020, the French State announced an exceptional package of €300Bn state-guaranteed loans (“PGE”) to support SMEs during the Covid-19 crisis. Following the amendment voted at the end of April 2020, lending marketplaces such as October were eligible to participate to the French state-guaranteed loans scheme and offer state-guaranteed loans to eligible borrowers.

Since the launch of the first state-guaranteed loan on the October platform in June, 68 French state-guaranteed loans were funded by institutional and retail lenders for a total amount of 13.167.000€ and new loans will be granted in the coming months, following the government announcement to extend the guarantee program until June 2021.

In December 2020, the French government also announced a modification of the repayment scheme for these projects. Businesses that wish to delay the capital repayment of their state-guaranteed loan can now request a 1-year additional deferral to their creditor, who will choose to grant it or not.

The initial repayment scheme

The state-guaranteed loans are different from the standard loans published on October. The characteristics of these loans (duration, interest rate) have been set by the French government.

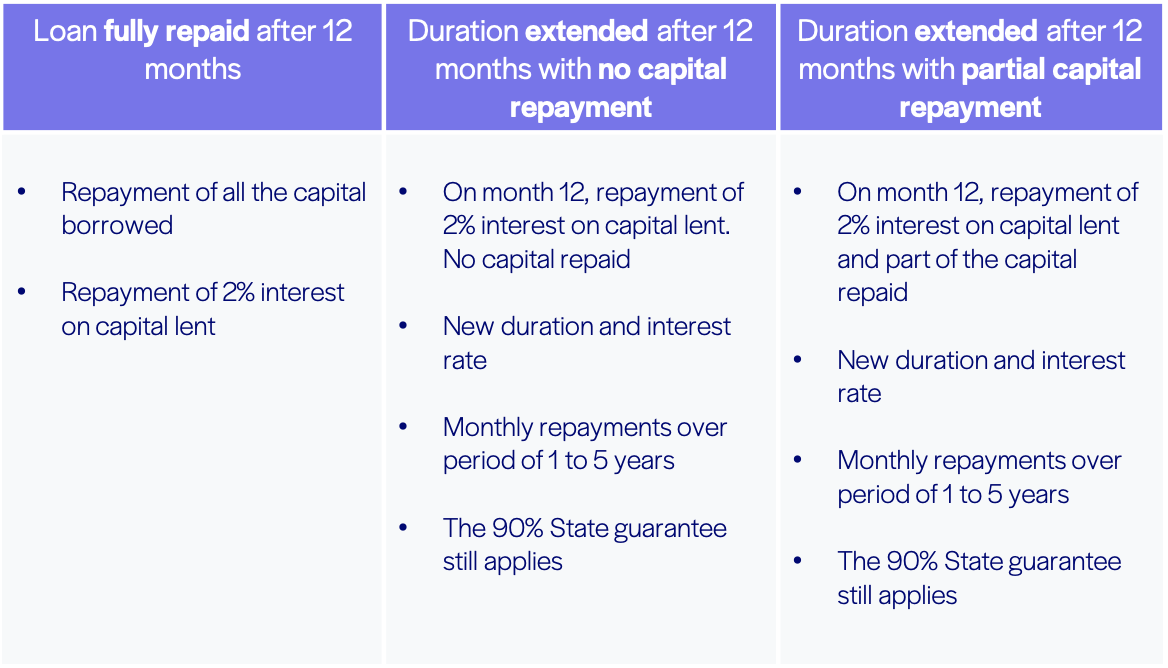

French state-guaranteed loans are initially 12-month deferred loans with payment of interest (2%) and principal at the end of the loan. However, what makes the state-guaranteed loan unique is that the borrower can decide to extend their loan after the first 12 months, with a higher interest rate. At the end of this period, the borrower has the following 3 options :

The new repayment scheme

Following an announcement from the French Ministry of the Economy and Finance on December 14, 2020, all companies that were granted a state-guaranteed loan, regardless of their activity and size, can apply for an additional one-year deferral to start repaying the capital of their state-guaranteed loan.

If a borrower wishes to extend their loan, they can now ask October for the extension of the deferral period for another 12 months, during which the company would repay only interest every month, followed by an amortisation period of up to 4 years, during which the borrower would repay both capital and interest (i.e. the maximum duration to fully amortise the loan remains 5 years).

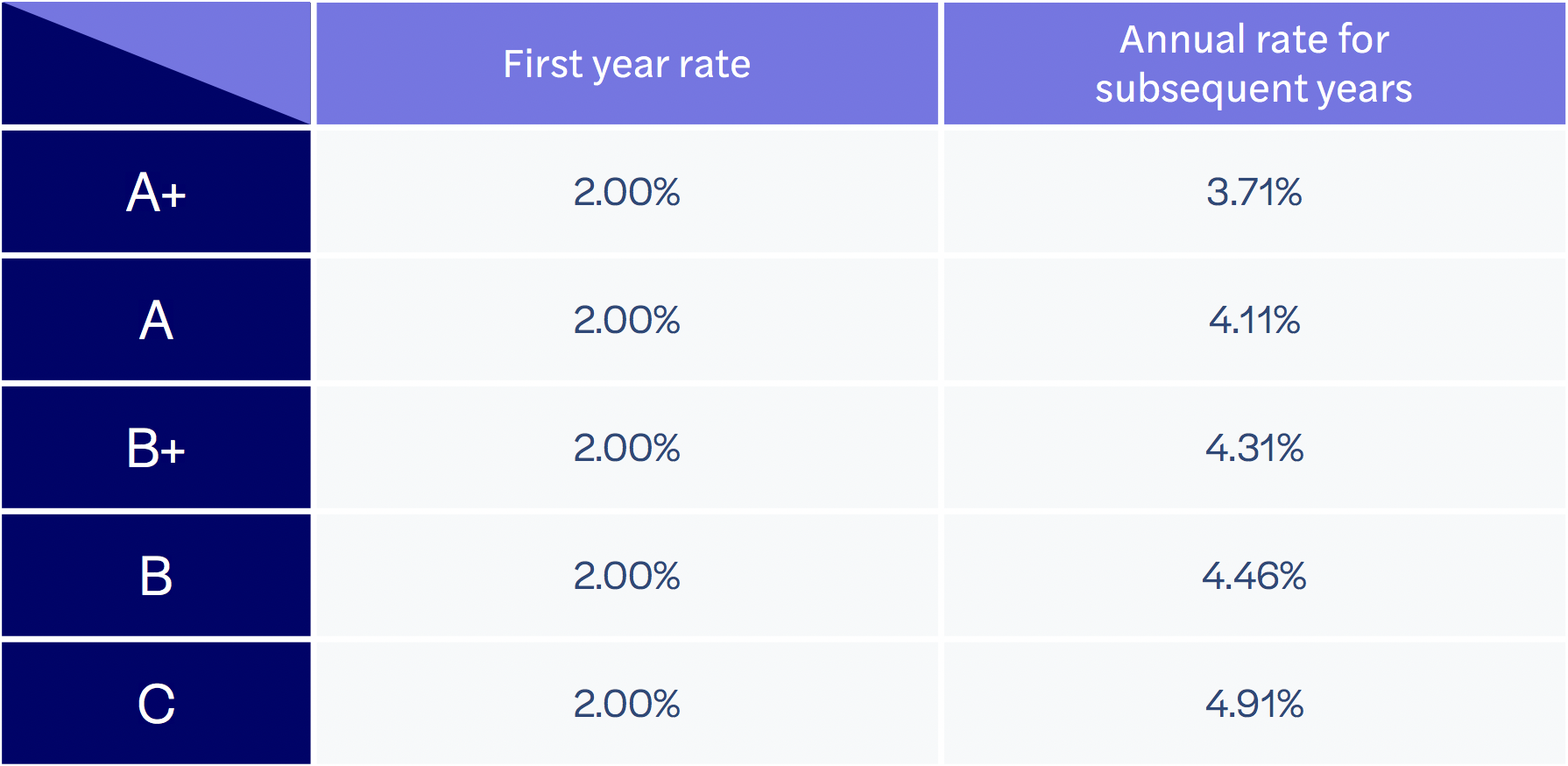

The interest rate applicable during the additional 12-month deferral period is between 3.71% and 4.91% depending of the project rating (see table below):

When applying for the extension of the deferral period, the borrower will also have to indicate whether they will repay their loan immediately at the end of the deferral or whether they will spread the repayments over several years (in that case, they will also need to state the duration of the amortisation). If the company decides to spread the capital repayment after the extra deferral period, the loan will be repaid through annuities, with an interest rate comprised between 3.71% and 4.91%.

⚠️ Contrary to the extension of the amortisation period for a period of 1 to 5 years, this extra deferral period is not granted automatically.

- October will study the applications on a case-by-case basis and will verify the company’s need to request the extra deferral period by requesting additional documents, studying the impact of Covid-19 on the company’s sector…

- If the October Committee accepts the application, we will ask the October lenders to vote.

What does it change for the retail lenders?

If a company you financed requests the extension of the deferral period for their state-guaranteed loan:

- You will be notified by email and request to vote on the additional deferral period

- If the majority of institutional and retail lenders (in volume lent) votes in favour of the additional deferral period, the extra 12-month deferral will be granted and the company will only repay interest during that time. The interest rate you will receive will be increased.

- The new repayments will be displayed in your portfolio, on the Future Transactions tab.

From June 2021, we could start receiving some extension requests from borrowers who were granted a state-guaranteed loan.

Not all company will request the additional deferral period. Nevertheless, you need to be prepared in case that happens. The October team is at your disposal for any questions you may have relative to this change.