The slowdown in the eurozone economy that followed Lehman Brothers’ bankrupcy in 2008 and the sovereign debt crisis of 2011, had serious repercussions on the supply of loans from the banking system to european firms. However, the extent of this phenomenon has not been homogeneous. The credit systems that have suffered the most are those who’s structure was already weakened by the increase of non-performing loans.

Sergio Zocchi, CEO of October Italy: “The ability of credit institutions to free up resources for the benefit of the real economy is limited by several factors, including a high ratio between non-performing loans and assets. The use of alternative financing channels allows companies to provide themselves with a capital structure that is less exposed to the banking channel. Complementary instruments to bank credit are also gaining ground in Europe”.

Restriction of bank credit: a European phenomenon

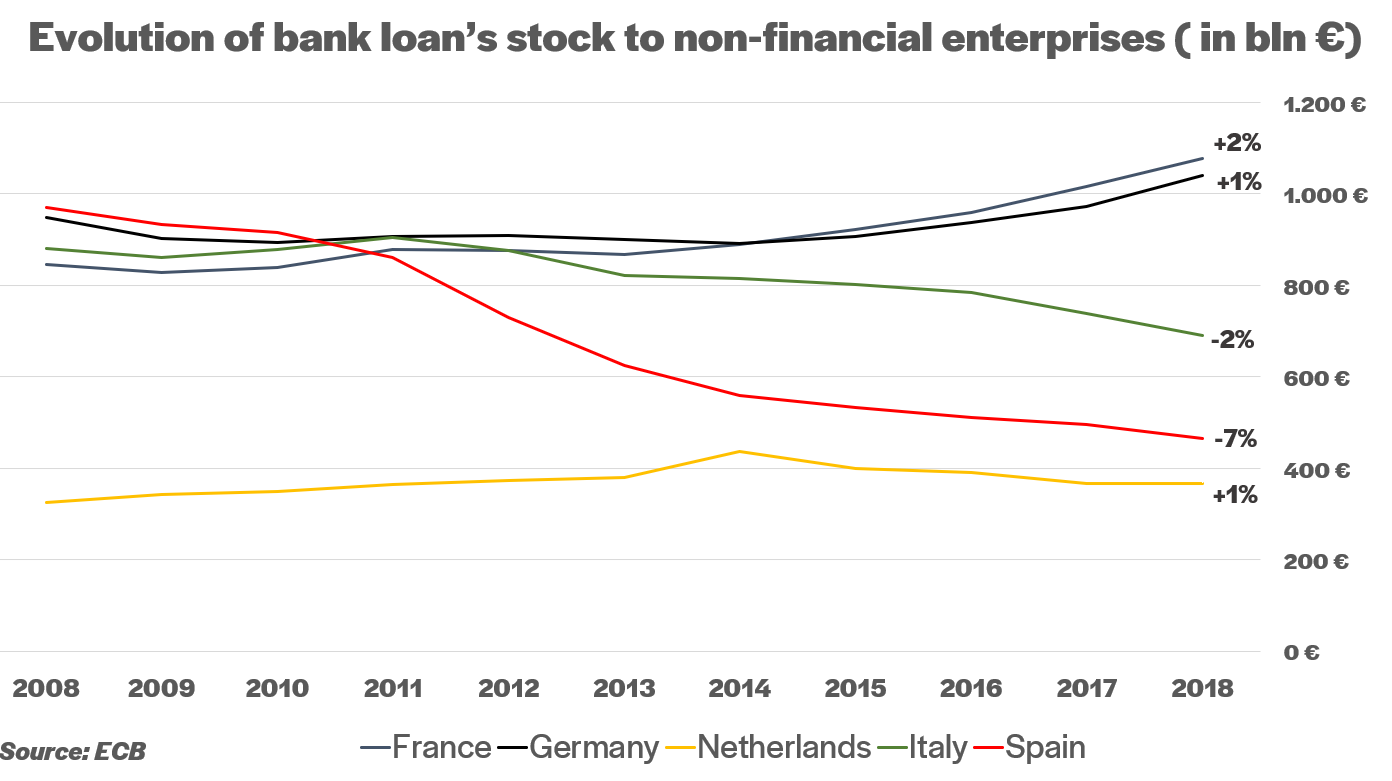

In order to understand the extent of credit crunch in Europe, we focused our analysis on the ECB’s data on the stock of corporate lending by French, German, Dutch, Italian and Spanish banks in the timeframe between 2008 and 2018.

The reduction in the supply of bank credit has affected several economies within the European Union. But as the credit institutions of France, Germany and the Netherlands were able to react to the 2008 and 2011 crisis by keeping the overall stock of loans stable (or increasing it), the same thing cannot be said for the Italian and Spanish banking system. Here, as a matter of fact, the overall volume of loans to non-financial firms has shrunk by an average annual rate of 2% and 7% respectively.

The burden of non performing loans

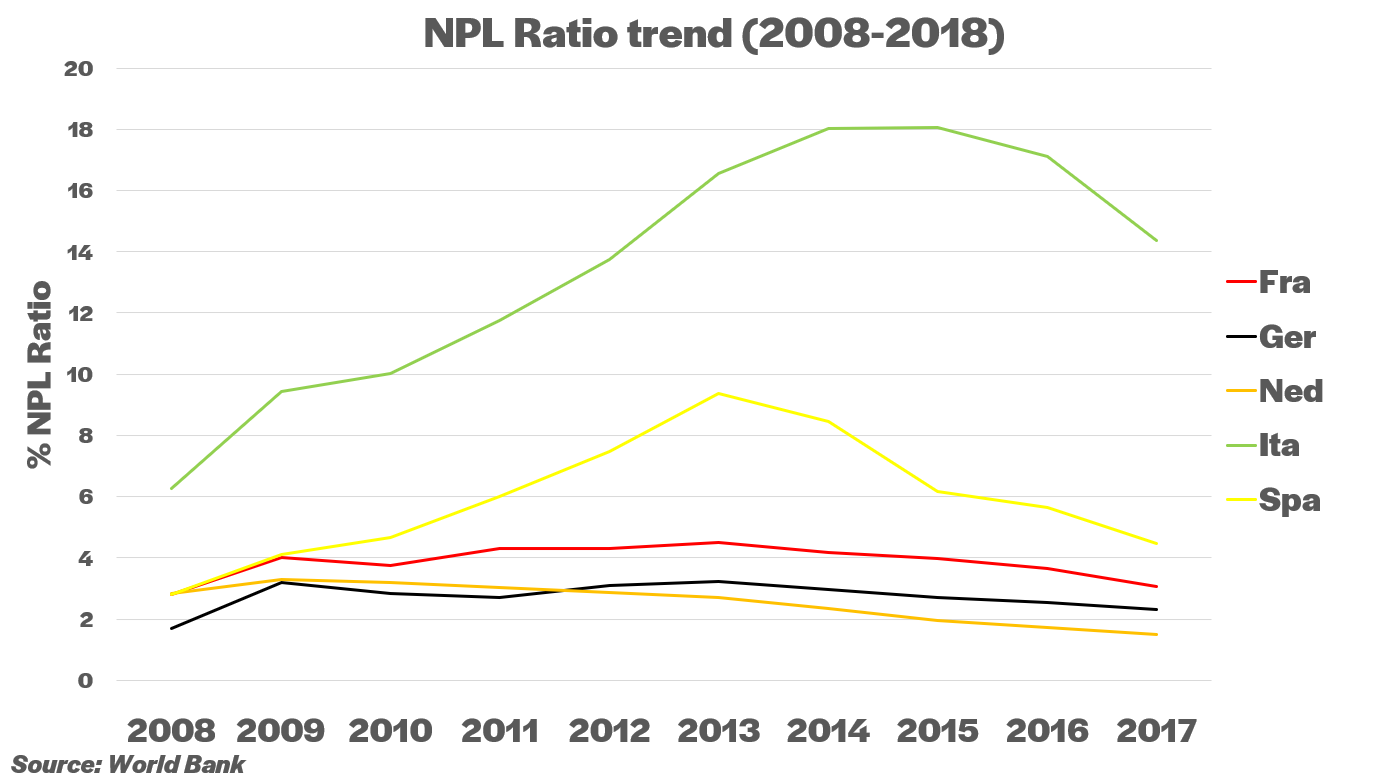

How come some European countries experienced positive rates while others have suffered the opposite trend? A first explanation can be found in the different exposure of national banks to non-performing loans. Non-performing loans are defined as credit exposures where banks are experiencing difficulties in recollection.

In Germany, France and the Netherlands the ratio of non-performing loans to total bank assets known as NPL ratio remained under control. In Italy and Spain such ratio increased progressively, reaching alarming thresholds of 14% and 4.5% (source: World bank). In both countries, such increase reached its peak especially in 2010, right when the first significant signs of a reduction in loans to corporations became apparent. This data highlights the existence of a correlation between NPL’s and the reduction in new loans granted by the banking channel. The heavy presence of non-performing loans forced credit institutions to a write-off the value of such loans in their balance sheets, from which they were able to protect themselves only by reviewing loan conditions and reducing new disbursements. This situation was also negatively affected by the introduction from the European legislator of increasingly stringent capital and income requirements.

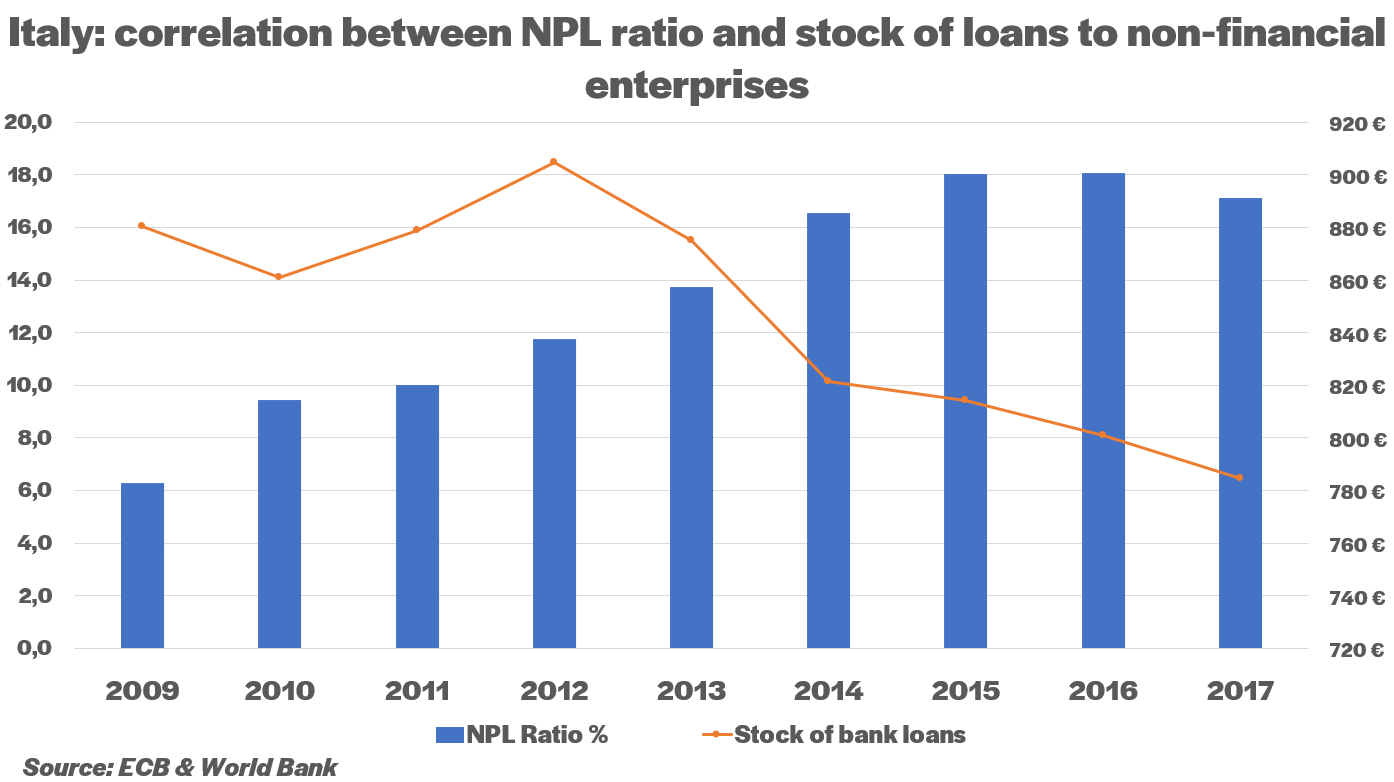

The stock of NPL’s, together with increasingly stringent accounting requirements, has therefore forced banks, specially those based in Italy and Spain, to adopt stricter criteria on the granting of credit, leading to more difficult acces to finance specially to businesses. According to data from PWC, in the first half of 2018 in Italy the “Corporate & SME” segment accounted for the majority of NPL’s, with an incidence of 68%. The importance of non-performing loans and their link with lending activities have clearly affected especially a country like Italy in which, at the end of 2017, the ratio of NPL’s to total assets of the banking system stood at 14%, compared to an average of 3.72% NPL ratio amongst European countries.

The progressive increase in non-performing loans held in the portfolio of Italian and Spanish credit institutions is motivated not only by the prolonged recession that has involved the euro zone. If the reasons were exclusively of macroeconomic origin, it would not be explained why banks in other European countries, also affected by the 2008 and 2011 crisis such as France or Germany, have instead seen a reduction in the incidence of NPL’s on their balance sheets. It should be noted that the increase in NPL’s has also been caused by “systemic” factors of this countries such as, for example, the inefficiencies in debt recovery, the slowness of civil court proceedings or the absence of a secondary market for non-performing loans that would allow Italian or spanish banks to sell these loans, freeing up resources for businesses and the real economy.

The entrepreneur’s concerns relating the access to finance

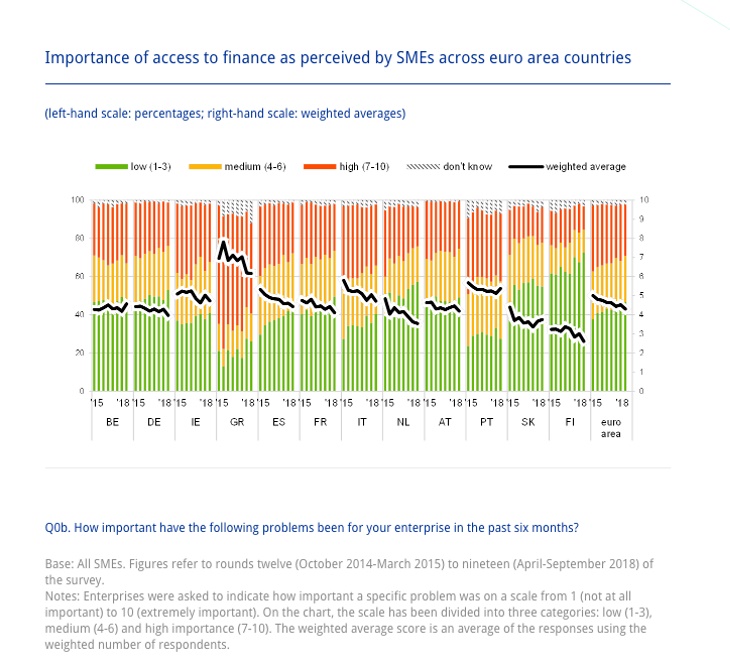

It is interesting to note that there are different perceptions among European entrepreneurs regarding the issue of access to credit. The ECB’s ‘Survey on the access to finance of enterprises‘ shows that in countries with stronger financial systems, which have managed to maintain their stock of loans to businesses and their non-performing loans at stable levels, access to credit is not a major cause for concern. Businesses were asked to indicate the importance of access to credit on a scale from 1 (not at all important) to 10 (extremely important). Greek SMEs consider access to finance as the main cause for concern (with an average rating of 6.2), followed by Portuguese SMEs (5.4) and Italian and Irish SMEs (both at 4.7), compared to an euro-area average of 4.3.

Opportunity and challenge

Many good businesses are not able to meet the strict requirements for credit by banks. In this case alternative financing provides a solution. October is able to operate in this gap all around Europe.

Of course, the challenge is to keep the percentage of NPLs in the October portfolio to a minimum. Through comprehensive credit analysis October is confident it will manage and filter the good businesses from the bad ones. State initiatives like the Fondo di Garanzia help regain trust in financing businesses as well.