Last week, we hosted a webinar in each country where October is active to give our lenders insight into the French State-guaranteed loans and resolve their doubts about their purpose and their conditions. More than 300 lenders registered to these webinars and shared their questions with our Lenders Team. Thank you to all of you who participated in the webinar! If you were not able to attend or if your question could not been answered during the live webinar, you can find in this article the answers to the main questions we received and the link to watch the replay in your language.

Do you offer state-guaranteed loans in other countries than France? What are the differences between each guarantee program?

October participates in the French, Italian and Dutch state guarantee programs, but the conditions of the loans differ depending of the country:

- In France, borrowers benefitting from the French State guarantee initially receive a 12-month deferred loan at 2%, which can be extended up to 5 years with a higher interest rate. The guarantee covers 90% of the outstanding capital in case of default.

- In Italy, the “Fondo di Garanzia PMI” guarantee scheme put in place by the Italian government only applies to loans financed exclusively by institutional investors and covers up to 90% of the outstanding capital. October actively participates in this program to refinance elegible loans of our existing portfolio and to grant new loans to Italian borrowers elegible to the guarantee.

- In The Netherlands, October participates in the ****Dutch State guarantee program. The guarantee is only made available to eligible companies once other government measures have been used, and covers approximately 65% of the outstanding capital. In the Netherlands, likewise Italy, the interest rate of the state-guaranteed loans is not capped and is determined by the Credit Committee of October.

Finally, In Spain and Germany, where lending platforms are not allowed to participate in state guarantee programs, October continues to support SMEs with non-guaranteed loans, based on a thorough credit analysis to assess the impact of Covid-19 and the timeline to go back to a certain level of normality.

Why is the current offer almost only made of state-guaranteed loans?

In France, the borrowers’ demand is driven almost exclusively by state-guaranteed loans. Borrowers are currently looking for solutions to address their liquidity needs and logically prefer to borrow with low interest rates. The 90% coverage offered by the French State is designed to compensate for this shortfall on the lenders’ side.Nevertheless, we keep on working to publish standard non-guaranteed projects on the platform, in particular in Spain and in the Netherlands. As of October 2020, we funded approximately 110 standard projects for a total volume of € 49M and 170 guaranteed projects, representing a total amount of € 36M.

- Why cannot retail lenders lend to Italian state-guaranteed projects?As mentioned above, the Italian State guarantee program (Fondo di Garanzia) only covers the principal of loans financed entirely by institutional and professional investors of the October Funds. This is the reason why the Italian state-guaranteed projects are not available for retail lenders.

- Who determine the interest rate of the French state-guaranteed loan before and after its extension? Is it the borrower or October?

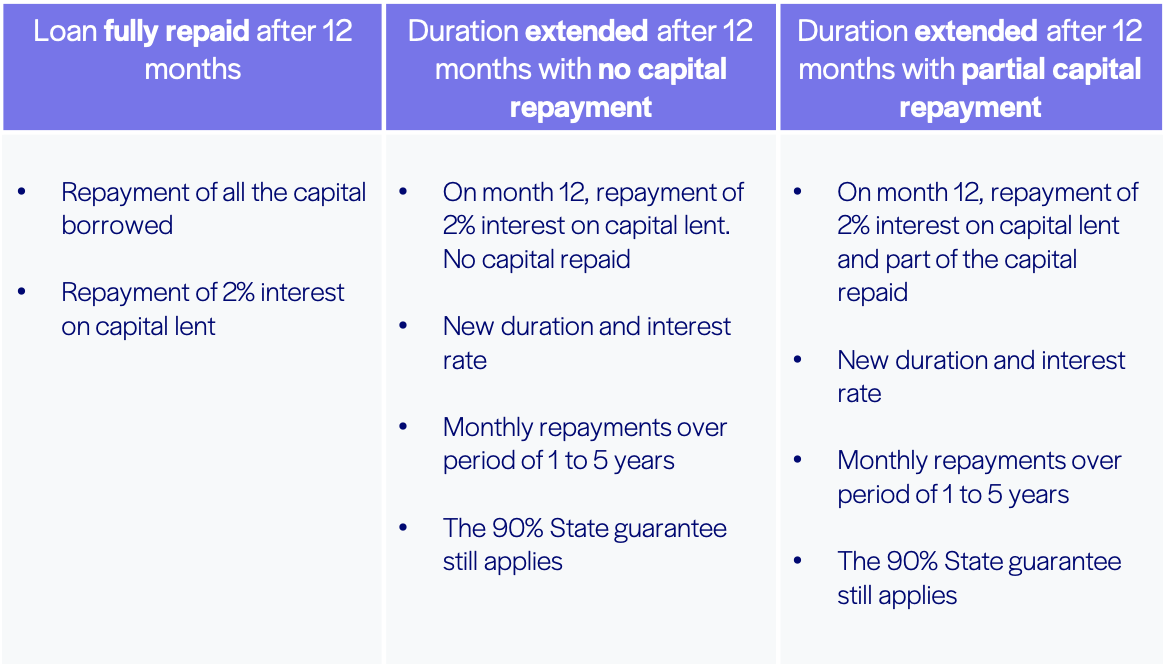

Before talking about how the interest rate is determined, let us recall the way the French state-guaranteed loans work.After the first 12 months, the company can decide between different options: they can either repay the full loan (principal and interest), repay partially (part of the capital and interest) or repay only the interest. In the last 2 cases, the loan will be extend for an additional period of 1 to 5 years with a higher interest rate and the guarantee will keep applying for the whole period.It is the company is who decide to extend it or not and for how long. The interest rate of 2% applicable during the first 12 months of the loan is framed by an agreement by the French Ministry of Economy and Finances and the lending platforms.

The interest rate of 2% applicable during the first 12 months of the loan is framed by an agreement by the French Ministry of Economy and Finances and the lending platforms.

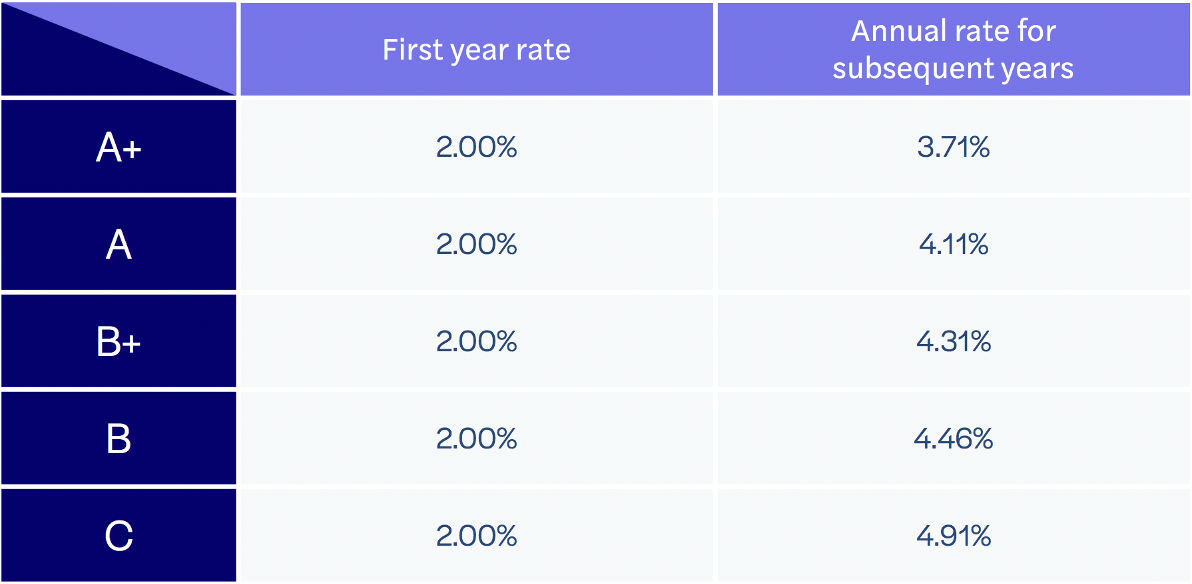

The higher interest rate applicable in case of extension is determined by October. After the 12-month initial period, the interest rate paid by companies will depend on their credit score (from A+ to C).

Why do most French state-guaranteed loans have a B or C score?

Most state-guaranteed loans published on the platform are Instant Projects. These projects are analysed by Magpie, an automatic borrower loan eligibility assessment model. Magpie is built using machine learning algorithms on large amounts of data collected by October over the past 5 years across different countries. It estimates the probability of payment default (PD) of a company and scores it from a scale going from 1 to 5. Instants Projects will always have a credit score between B and C. Since Instant Projects are analysed without human intervention, they may carry a higher level of risk which is reflected on their credit score.

Finally, since Credit analyst are not involved in the underwriting of Instant Projects, the project description is standardised and do not include the analyst’s opinion. The role of analyst for these projects is to verify the company’s eligibility for a state guarantee and performing some compliance checks.

If the company decide to extend the loan, can I request an early repayment?

No, on that matter, French state-guaranteed loans work the same way as standard projects. Once the company has received the funding, you have to wait until the loan is fully repaid to get your investment back. Also, you cannot sell that loan, as secondary markets are not authorised for this type of assets for regulatory reasons. Nevertheless, while a project is still going on October, you can cancel your loan.

In one word, if you lend to a company benefiting from the French State guarantee, you have to assume the risk in case the loan is extended and to wait until the loan is fully amortised to receive the total amount of capital.

Is the loan covered even in case of extension?

Yes, as you can see on the table presented above, the loan is covered by the French State guarantee during all the period even in case of extension.

There would be only 2 cases for which the guarantee would not apply:

- If the company goes into bankruptcy in the first 2 months (so far, no company we have funded has been in that situation),

- If the French State goes into bankruptcy, which is unlikely but has to be taken into account.

Can the borrower repay the loan earlier than 12 months?

For standard projects, the October contract authorise borrowers to do an early repayment at any point. Depending of the contract, the company may or may not have to pay an early repayment fee.

In the case of French state-guaranteed loans, our contract does not allow the borrower to do an early repayment during the initial 12-month period. Borrowers are allowed nevertheless to repay their loan early passed this period provided they pay the early repayment fee. However, based on the current economic context, we do not expect companies requesting a French state-guaranteed loan to repay early.

We hope that you have a better idea about the projects with French State-guarantee and that you feel more comfortable when you lend to these projects.